Asset allocation is a crucial concept in investing. It involves dividing your investments into different categories known as asset classes. These asset classes typically include stocks, bonds, cash, and other types of investments.

What is Asset Allocation?

Definition: Asset allocation is like putting your eggs in different baskets. It means spreading your money across various types of investments. Instead of putting all your money into one type of investment, you diversify by investing in different things.

Why is Asset Allocation Important?

Importance: The main reason for asset allocation is to reduce the risk of losing all your money if one type of investment performs poorly. By spreading your investments across different asset classes, you can protect yourself from big losses.

Asset allocation is also important for targeting your investment goals. Different types of investments offer different levels of risk and potential return. By allocating your assets wisely, you can balance risk and potential reward to meet your financial objectives.

How Does Asset Allocation Work?

Asset allocation involves deciding how much of your money to put into each type of investment. This decision depends on factors like your age, financial goals, risk tolerance, and how long you plan to invest.

Asset Classes: Asset classes are categories of investments that have similar characteristics and behave in similar ways. Common asset classes include:

- Stocks: Ownership in a company.

- Bonds: Loans to governments or corporations.

- Cash: Money in savings accounts, CDs, or money market funds.

- Real Estate: Property and land.

- Commodities: Raw materials like gold, oil, or agricultural products.

Table of Contents

Toggle

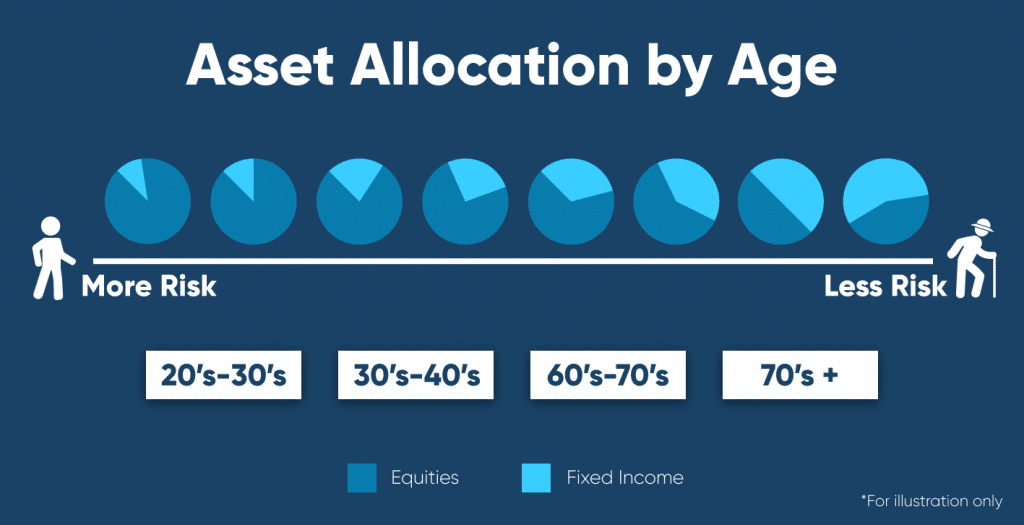

Understanding Age and Risk Tolerance

Younger Investors (20s-30s)

Young investors in their 20s and 30s typically have a longer time horizon for their investments. This means they can afford to take more risks because they have more time to recover from any losses. Here are some key points to consider:

- Higher Risk Tolerance: Younger investors usually have a higher risk tolerance. This means they are more willing to invest in riskier assets like stocks because they have the time to ride out market fluctuations.

- Allocation Towards Stocks: Since they have a longer investment horizon, younger investors may allocate a larger portion of their portfolio towards stocks. Stocks have higher growth potential over the long term, which aligns with their investment goals.

- Related Entities: Younger investors often focus on long-term goals such as retirement planning. They are concerned with building wealth over time to secure their financial future.

Middle-Aged Investors (40s-50s)

Middle-aged investors, typically in their 40s and 50s, are in a different stage of life compared to younger investors. Here's what you need to know about their risk tolerance:

- Moderate Risk Tolerance: As investors approach middle age, their risk tolerance may become more moderate. They are more concerned with preserving the wealth they have accumulated rather than taking significant risks.

- Balance Between Growth and Income: Middle-aged investors often seek a balance between growth and income generation. They still want their investments to grow, but they also need to generate income to support their current lifestyle and future retirement.

- Related Entities: Wealth accumulation and retirement planning are key focuses for middle-aged investors. They are working towards building a nest egg that will sustain them during retirement.

Older Investors (60s+)

Investors in their 60s and beyond have different priorities and considerations when it comes to risk tolerance:

- Lower Risk Tolerance: Generally, older investors have a lower risk tolerance, especially as they near retirement age. They are more concerned with preserving their capital rather than chasing high returns.

- Focus on Income and Capital Preservation: Older investors often shift their focus towards income generation and capital preservation. They prioritize investments that provide a steady stream of income and protect their wealth from market volatility.

- Related Entities: Retirement income and income-generating investments are crucial for older investors. They rely on these investments to sustain their lifestyle during retirement.

Understanding Asset Allocation Rules

Asset Allocation Rules: A Starting Point

Asset allocation rules provide guidelines on how to divide your investments among different assets. They are not strict formulas but serve as starting points to help investors make informed decisions.

A. Rule of 100

The Rule of 100 suggests subtracting your age from 100 to determine the percentage of your portfolio that should be allocated to stocks. For instance, if you're 30 years old, you might allocate 70% (100 - 30) of your portfolio to stocks.

B. Rule of 110

As lifespans increase, the Rule of 100 may not provide enough exposure to the growth potential of stocks. The Rule of 110 adjusts this by subtracting your age from 110, allowing for a slightly higher allocation to stocks.

C. Importance of Asset Allocation

It's crucial to consider these rules alongside your risk tolerance. While asset allocation can help manage risk, it's essential to ensure that your investment strategy aligns with your comfort level with market fluctuations.

When determining your asset allocation strategy, consider using tools like risk tolerance calculators and investment planning tools. These resources can provide insights into your risk tolerance and help tailor your investment approach accordingly.

By understanding asset allocation rules, risk tolerance calculator and investment planning tools, investors can create a balanced portfolio that aligns with their financial goals and risk preferences.

Understanding Additional Factors Beyond Age for Investing

When it comes to investing, age is just one piece of the puzzle. Several other factors play a crucial role in determining the best investment strategy for you. Let's delve deeper into these factors:

Investment Goals

Your investment goals are like your destination on a roadmap. They give direction to your investment journey. Whether you're saving for retirement, planning for a down payment on a house, or building an emergency fund, your goals shape your investment decisions.

Financial Situation

Your current financial situation sets the stage for your investment journey. Factors such as your income, debts, and the size of your emergency fund are essential considerations. Your income determines how much you can invest, while managing debts ensures you have more resources to allocate towards investments. An emergency fund provides a safety net, allowing you to invest with peace of mind.

Risk Tolerance

Investing involves risk, and everyone has a different comfort level when it comes to dealing with it. Your risk tolerance reflects how much market fluctuation you can stomach without losing sleep. Some investors are comfortable with high-risk, high-reward investments, while others prefer a more conservative approach. Understanding your risk tolerance helps you choose investments aligned with your comfort level.

Investment Timeframe

The timeframe for your investments is another critical factor to consider. How long until you need the money you're investing? Short-term goals may call for different investment strategies than long-term ones. For example, if you're saving for a down payment on a house in the next few years, you might opt for more stable, low-risk investments. On the other hand, if you're investing for retirement decades away, you might be more inclined to take on higher risks for potentially higher returns.

By considering these additional factors beyond age, you can develop a personalized investment plan that aligns with your goals, financial situation, risk tolerance, and investment timeframe. Remember, investing is not one-size-fits-all. It's about finding the approach that works best for you and your unique circumstances.

Conclusion

Finding the right asset allocation is an ongoing process, not a set-it-and-forget-it decision. As your life circumstances and goals evolve, so should your investment strategy. Review your asset allocation periodically and make adjustments as needed. Remember, there's no one-size-fits-all answer.

For a more personalized approach, consider consulting with a financial advisor. They can help you assess your risk tolerance, investment goals, and create a customized asset allocation plan that aligns with your unique financial situation.